The big picture

- Strong market returns have continued, however, the drivers of returns have changed over the last year, pivoting away from the US and Artificial Intelligence (AI).

- Developed markets are expecting earnings to broaden from the returns from AI that have dominated over the last three years. However, headwinds may lead to subdued and volatile returns for major indices.

- Opportunities increase from active management in developed markets and in other asset classes, including emerging markets, global listed infrastructure and global listed property.

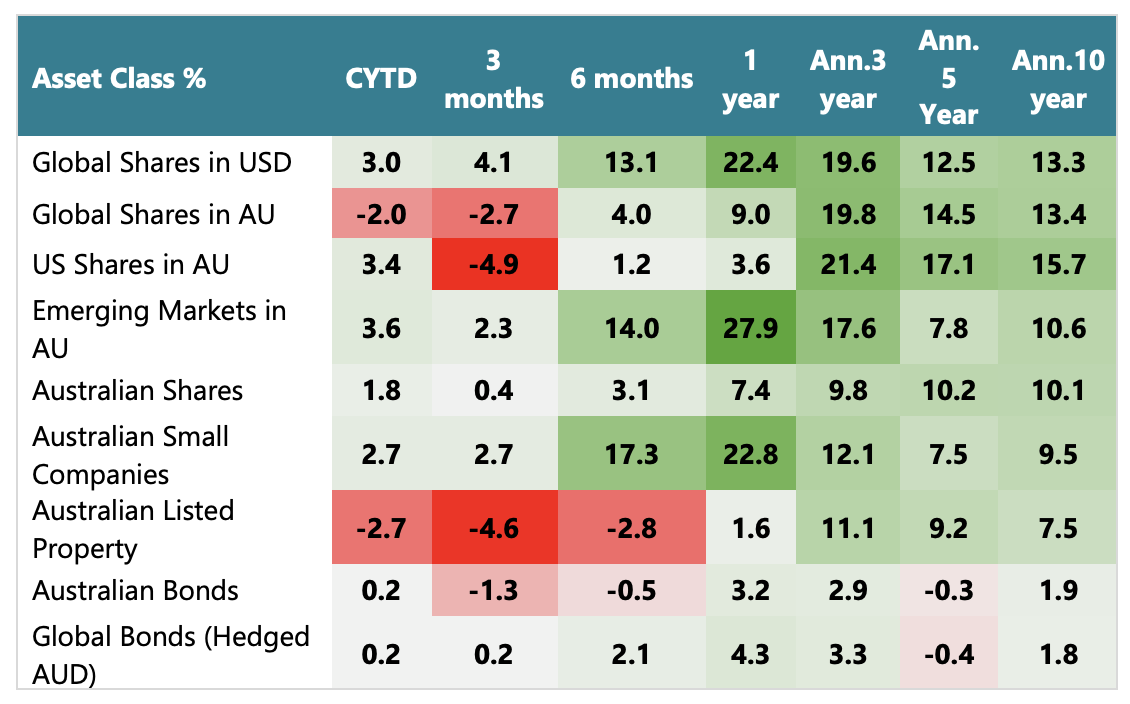

How Investments Performed (to January 31, 2026)

The share markets provided good returns in 2025, which continued into 2026, although the ride was at times bumpy. This caps off a three-year period of unusually positive returns.

Global shares did very well. Surprisingly, and despite the strength of the US economy, the US share market lagged much of the developed world. Investors are beginning to question whether AI companies’ profitability can be maintained amid substantial capital expenditures. The stronger Australian and sharply weaker US dollar significantly reduced returns for Australian investors in global shares.

High global liquidity, along with extreme risk sentiment, has led to speculative behaviour in many markets. In the US and in Australia, quality companies were sold off despite many having solid earnings outlooks.

Emerging markets are a major investment theme, delivering very strong returns.

In Australia, the Resources sector (especially gold and base metals) drove returns in the past year, a significant turnaround from the prior year, when led by banks and technology. In January the Healthcare sector rebounded after being the worst performer in 2025.

Australian small cap stocks delivered impressive returns over the past year, a reversal from 2024 when large cap stocks dominated. Listed property dropped sharply due to the expected RBA rate hike, which occurred in early Feb 2026.

Australian bond returns were below cash due to rising yields, although global bonds exceeded the cash rate of 3.6% over 1 year.

The numbers (to January 31, 2026)

Looking ahead

We’re positive about 2026 overall, with decent earnings expected. However, possible challenges include: the developed world (excluding the US) slowing; high sovereign debt levels; inflation re-emerging in the US and Australia; elevated valuations; and geopolitical tensions.

Australia’s economy shows some improvement with rising business investment and consumer confidence (though from low levels). However, productivity remains low, manufacturing confidence is very weak, and the recent spike in inflation and the increase in interest rates add to cost-of-living pressures.

Our investment recommendations are positive on growth assets and quality credit but focused on active management. Additionally, sub asset classes are showing relative value and appear better positioned for this stage of the cycle.

Conclusion

In times of uncertainty, we suggest:

- Diversification across different asset classes.

- Remain flexible and incorporate active management.

- Review currency hedging strategies.

- Use bonds and high-quality credit for income and stability.

- Regularly rebalancing your portfolio to maintain target allocations.

- Seek to incorporate some inflation protection through listed global property and infrastructure.

The information contained in this article is general information only. It is not intended to be a recommendation, offer, advice or invitation to purchase, sell or otherwise deal in securities or other investments. Before making any decision in respect to a financial product, you should seek advice from an appropriately qualified professional. We believe that the information contained in this document is accurate. However, we are not specifically licensed to provide tax or legal advice and any information that may relate to you should be confirmed with your tax or legal adviser.